Info på AOJ.

-

AOJ: 1-page pitch

Mcap: $280m

TL;DR:

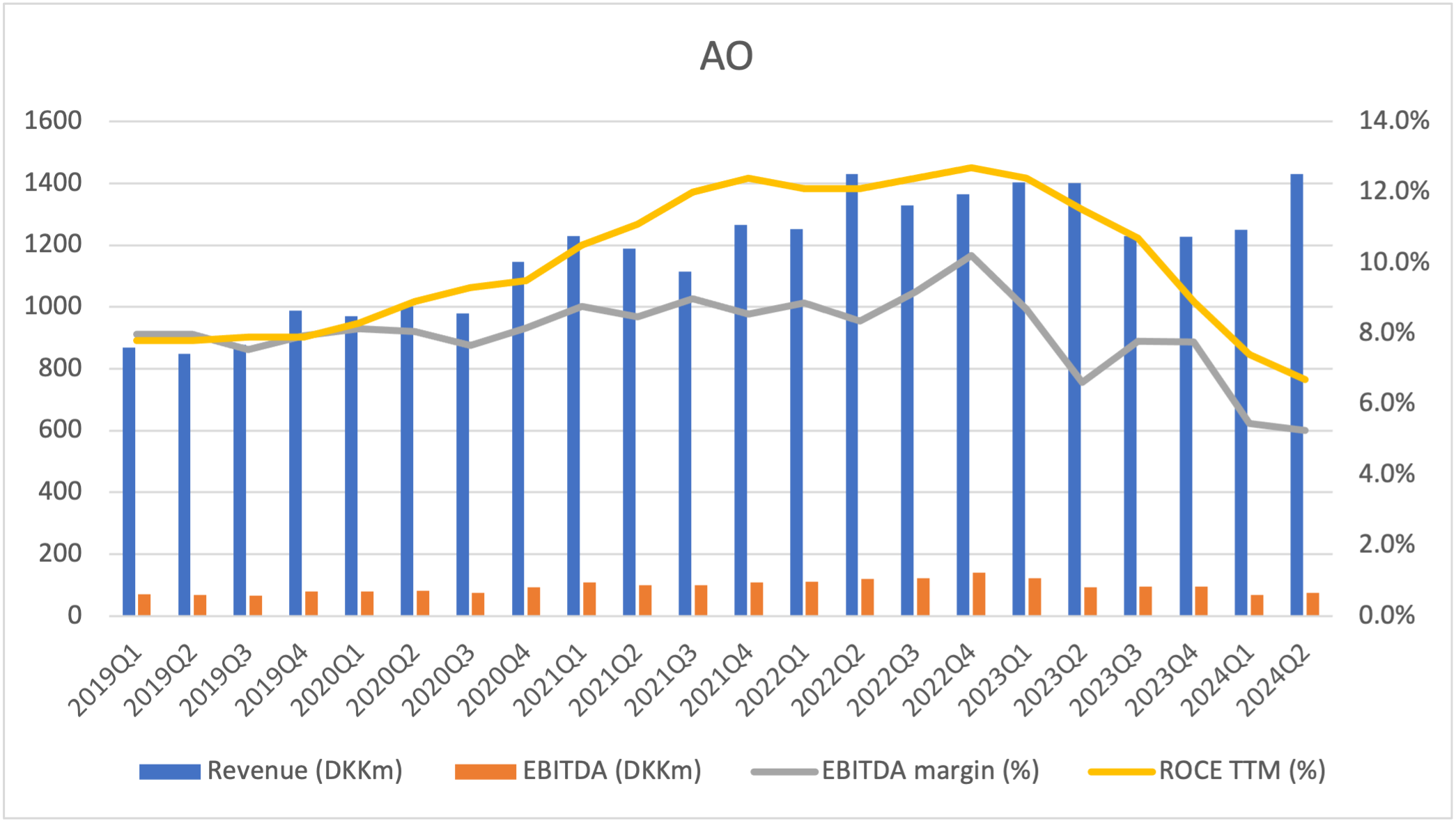

- ev/ebit ~7-8x on depressed earnings, 6-7% dividend & real estate +50% of market cap as a valuation cushion

- extensive investments through 2018-2023: entering the next up-cycle (2024-2027?) highly efficient, peak market share, peak capacity and no major capex needs

Business:

-

Market leading B2B Heating, Plumbing, Electric & Water Supply distributor in Denmark (+28 000 business customers)

-

global peers: Ferguson (US), Ahlsell (SE), Onninen (FI), Wesco (US), Dahl (DK)

-

Market leading B2C Online Plumping/Heating/Sanitary in Denmark (+430 000 private customers)

-

global peers: BHG Group (SE), Victoria Group Plc (UK)

-

EU Taxonomy aligned assortment

-

Approx. 70% of revenue is towards repair, maintenance and renovation i.e. low-mid cyclical

-

Customers (schools, industrials, residentials, commercials, etc.) face asset impairment without maintenance & repair

Distribution 101:

- Academic literature names it a "Fortress Position" to be #1-2 in a single country (almost impossible to dismantle)

- Provides +28 000 tradesmen (plumbers, electricians, carpenters, etc) with +600 000 SKUs from +2 500 manufacturers

- 101: Wholesalers offer economic benefits by consolidating goods from various manufacturers, allowing tradesmen to access a wide range of products in one place. Their bulk purchasing power enables cost efficiencies, providing tradesmen with competitive prices while also offering manufacturers a streamlined distribution channel, ultimately contributing to a more efficient and cost-effective supply chain.

Tech Leadership:

B2B:

-

Automated central warehouse (2018 & exp. 2022) enabling 60 minute delivery to the largest cities.

-

SSI Schaefer Shuttle state-of-the-art equipment inside i.e. scale without additional manpower

-

Revenue per full-time employee up +36% 2018-2021

-

2015-2022: 6 years of market share gains & 2% p.p. operating-margin improvement

-

'AO365' = +51 unmanned big box stores open 24 hours per day 7 days a week

-

'AO365' covers 95% of Denmark within 30 minutes drive

-

'AO365' plumber gets a immediate water-leak job: drives by a AO365; scans all the installation supplies he needs with an app; puts it on credit; carry the supplies to his truck; done

-

'AO365' removes the need for most installers to carry inventory i.e. high switching costs/moat

B2C:

-

AOJ B2C passed +2 million visits in November 2023, ATH & +25% YoY.

-

Denmark B2C:

BilligVVS.dk

LavprisVVS.dk

LavprisEl.dk

LampeGuru.dk

Greenline.dk

CompletVVS.dk

LavprisVaerktoej.dk- Sweden & Norway B2C:

VVSochBad.se

LampeGuru.no

BilligVVS.noHard Assets:

- +$160-180m (+50% of mcap) of owned land, buildings & tier-1 equipment inside

- +30 locations

- Acquired plots throughout the 90s & 00s thus extremely good locations

- Competitors are now taking huge rental increases and/or closing down stores = AOJ Win/Win

Owners, Misc & End Game

-

Owner & Operator model, family owned 4th generation

-

Outsider-type CEO: history of substantial share buybacks, cancellation of shares, increased dividends and most importantly never diluted

-

Swedish giant Ahlsell spent fortunes for 10 years trying to enter & compete in Denmark, but failed and left

"Why so cheap?"

- Low free float

- AO had its first ever Analyst Coverage (BUY 55% upside) 2 months ago (October 2023)

- AO had its first ever Investor Presentation in Q1 2022

- AO had its first ever Conference Call in Q1 2022

(Why did a majority owner start with all this, at age 84? Does he maybe want to get interest and prices up for a sale...)

"Buyout?"

- The owner/CEO is 84 years old and have moved (tax & residency) to the US.

- The only son quit all operational roles, and the board, 14 years ago (no interest).

- The only son moved out of Denmark, sold his house in DK and is now a US resident.

- Family owners almost always want to settle company transition before passing

Summary:

-

Consumers have been reserved with discretionary spend for ~2 years

-

Upturn 2024-2027?

-

Falling interest rates in Denmark, Sweden & Norway throughout 2024-(?) - huge stock of floating rate mortgages

-

Buy a market leader at approx. 8-9x depressed net earnings (40-50% global peer discount) & 6-7% yearly dividend. Assuming the up-cycle arrives, you will have positive sentiment change for the sector AND actual earnings driving the shares upwards: multiple expansion + EPS growth.

-

Huge efficiency and capacity investments 2018-2023 that now are complete will most likely pave way for another step-up in margins the coming years, as per management guidance.

-

Optionality that Mr. Johansen decides to sell his company as there is no natural hier. Break-up value for PE (B2C, B2B & hard assets) should be absolutely massive - making a sizeable premium possible.

= Great R/R.

Hello! It looks like you're interested in this conversation, but you don't have an account yet.

Getting fed up of having to scroll through the same posts each visit? When you register for an account, you'll always come back to exactly where you were before, and choose to be notified of new replies (either via email, or push notification). You'll also be able to save bookmarks and upvote posts to show your appreciation to other community members.

With your input, this post could be even better 💗

Tilmeld Log ind